从九月二十七日澳洲聆讯结束,到十月二日, Alita 清盘人发出公告以来,相信很多不毛山的朋友都经历了不小的情绪波动。

感谢很多朋友参与讨论,提出点子,经过两天努力,结合大家见解基础上,我已经总结完成了下面这篇文章的撰写。

现在需要作的事,就是把它翻译成英文,送到恰当的人和机构手里,在事情没有定型之前,发出中小投资者的声音。不毛山历经波折,在最后结果到来之前,我们努力过,这辈子才不会后悔。

我尝试了一下,google translation 可以作大部分工作,但是还是需要英语水平到位的人,最好是 native speaker 对它进行最后调整。

我觉得 原文的翻译内容,可以发送到

- Canaccord Genuity 的相关律师团队。

- 澳洲的股票论坛,尤其是与不毛山相关的论坛。

此外,如果要发给 新交所 SGX 相关团队 的话,还需要把题目改成 Alita 中小投资者的声音,或者类似题目,然后在内容中去掉一些情绪化的东西,方便 SGX相关部门考虑。

在此,豹某呼唤热心朋友们, 志愿站出来,分工合作,收集相关机构团体的联系方式,承担翻译,修改 和 向相关人士和机构发送的任务。

也热切呼唤更多朋友参与到讨论中来,通过留言献计献策,看看我们中小投资者如何能够让自己的声音更大一点,让我们的利益得到更好保护,在一切还没有太晚之前。

豹某在此拜谢了。

【10月6日更新】

感谢热心朋友,十大诉求的英文版,已经在澳洲 Hotcopper 上了。

On 2nd October 2023,MN, the liquidators made an update to shareholders in SGX.

Leave with more question than answers.

Request liquidators for transparency and professionalism and kindly answer the following queries:

1. Disclose more information about the purchaser ACN 669 538 809 Pty Ltd, its date of establishment, registered capital, list of directors/officers.

2. According to the Singapore Catalist Rule 1006, the decision to approve the exemption clause is made after the valuation data is released and the SGX relevant authorities assess whether it is fair and reasonable.

3. The proponents need to clarifies their relationships with the other parties – independent assessor Deloitte (IER),creditor holder Austroid, lithium ore purchaser Hong Kong company YiHe, liquidator McGrath Nicol.

Is there any conflict of interest between these parties?

4. Publishes the current amount and composition of Alita’s debt and explain the mechanisms in place to prevent debt traps.

5. What capacity construction did Alita carry out during the period when it was seized by the creditor Chinese company’s Austroid, how much did it cost, how many shipment were exported, how many tons of lithium ore were exported, and what was the unit price and total price of ore?

6. What are the difficulties in explaining whether it is possible to bring in a third party to conduct further exploration of the minerals before winding up?

7. Discloses which companies other than Mineral Resource and its subsidiaries mentioned in the announcement have submitted proposals and for which/what reasons they are out. Explain specifically why their proposals are considered inoperable or lack certainty of implementation.

ACN 669 538 809,The offer from Pty Ltd and Mineral Resources was accepted, but we can see that in subsection 3.3, there is also a precondition for the transaction, does this precondition also mean that they also face the problem of certainty of execution?

(Hope that the liquidators will disclose more information on which companies have submitted proposals other than the Mineral Resources mentioned in the announcement, and which of the above reasons they have withdrawn).

Illustrate the circumstances in which a proposal is consideredinoperable.

8. Propose alternatives to the general meeting so that the liquidator and the shareholders can communicate directly to raise questions and explain doubts.

9. After the DOCA’s repeal, Alita has been freed from creditor Austroid, whether the Offtake Agreement between Austroid and YiHe is still in force. And is Alita be held responsible to pay taxes, if any, for the pricing offtake agreement between Austroid and YiHe? If Yes, Why so?

10. Please elaborate on the process of selecting an independent third party (IER) to issue a valuation report, which Deloitte has already issued in previous judicial proceedings. Please describe its selection process.

另外有个有利消息是, 距离不毛山 600米 的地方 Torque Metals Ltd (TOR)勘探得到很好结果,获得介于 10亿 到18 亿澳元之间的献议,献议者包括 MinRes 和嘉能可。

这个消息可以作为正面因素,一方面暗示不毛山矿脉,另一方面显示确实有多家公司对附近锂、钽资源有很高兴致。

ASX:TOR

The drill rig is currently spinning on-site and I can’t wait to see the spodumene

600 meters away from the Bald Hill mine which just last week got offered $1B to $1.8B from various buyers. MinRes plus Glencore

Up to 6% spodumene from rock chip sampling with many high grade samples obtained

Massive chunks of spodumene the director has been bringing to presentations to show off and also has a chunk in his office

Fully funded diamond drilling has commenced

Historical tantalum drilling with a maximum depth of 30m successfully intercepted abundant pegmatites with abundant spodumene noted in the drill logs as seen above.

The director knows exactly where to drill based off these historical results. Success is almost guaranteed. It is also interesting to note that Bald Hill originally was drilling tantalum and then discovered pegmatites with spodumene. The exact same scenario has happened here, wink wink only 600m away.

Bald Hill operators are currently drilling towards TOR tenements meaning the mineralization appears to be continuing to where we are, while at the same time we have already confirmed abundant spodumene.

Bald Hill buyers are eyeing nearby tenements and M&A is ripe. TOR already has mining licenses like WC8 which usually take years and heritage approvals so this discovery can progress very quickly. We are in the perfect position right now, a very unique one if you ask me. The buyers of Bald Hill will want to take us out really quickly once/if a discovery is confirmed. They can feed our ore into the Bald Hill processing plant.

感谢 Steven 网友的努力, 现在我们有下面的英文版本了。 我们尽可能把它发送给更多人和相关机构,越多人关注,获得公平的机会就越大,遭遇暗箱操作的风险就越小。

Time to check the table manner of Australians———–about Alita Resources (SGX:A40)

Alita’s abundant lithium resources make it a tempting target in the eyes of unscrupulous characters. Since the knowing of the lithium mine, it has faced lawsuits constantly. Along the way, it has experienced Jonathan Lim, Tjandra Adi Pramoko, and years of litigation between Austroid and Canaccord. After repeated twists and turns, it was originally thought that with the court ruling on September 27, 2023, in Australia, everything would settle down and Australian and Singaporean investors could get reasonable returns for a peaceful year.

Unexpectedly, a new announcement came out on October 2nd, a new company ACN 669 538 809 Pty Ltd as the purchaser appeared, the previously frequently mentioned Mineral Resources retreated behind the scenes and became the guarantor. At the same time, Deloitte was appointed to conduct valuation and issue an Independent Expert Report. However, in the situation where many questions have not been well clarified, it hurriedly set a timetable, requiring SGX to approve an exemption clause or delist Alita before October 27.

Under the current circumstances, delisting Alita will obviously make communication between investors and the company more difficult, which does not conform to SGX’s position of protecting small and medium investors and will also damage investors’ confidence in SGX.

Section B of the SGX Catalist Rules has clear requirements that selling the company requires shareholder approval. So once the requirement is exempted, investors will almost be removed from the game, with no chance to speak for their own interests in the contest concerning themselves.

In the fifth section of the announcement, a lot of space is used to explain the rationality of applying for the exemption clause. We understand the eager mood of the liquidator who sees profit coming. But as investors, we also have the right to demand more transparency and more in-depth explanations to resolve our doubts. Although it is difficult for Alita to hold a shareholder meeting under the current circumstances, it cannot be used as an excuse to close other possible communication channels.

As an investor, I have the following questions. I hope SGX can help us clarify them when responding to the Australian liquidator’s application for an exemption clause:

[1]

The first line of Section 2.2 of the announcement claims that the information about the purchaser and Mineral Resources in this section is provided by them, and the liquidator has not independently verified the accuracy and correctness of the relevant information.

We want to know whether the liquidator thinks the accuracy of the relevant information provided by the purchaser and Mineral Resources is unimportant at all?

If so, please explain why it is unimportant.

If not, please explain the difficulties in independent verification, and request the disclosing parties to provide more information for investors, media, and public to participate in verification together.

We note that the information provided by the purchaser and Mineral Resources is very limited. More needs to be supplemented in two aspects. The first aspect is more information about the purchaser ACN 669 538 809 Pty Ltd, such as its establishment time, registered capital, list of directors/executives. This information will help verify their subsequent claims. The purchaser’s name is so stylish and digital. In case it is just a short-lived existence purely for the parent company to do unspeakable things, then its directors/executives’ information is even more important and needs to be disclosed for future accountability.

The second aspect is that the relevant information provided by the purchaser and Mineral Resources only clears that they do not hold Alita’s shares and are not related to Alita’s directors/major shareholders, nor have they had any private transactions or arrangements with Alita’s directors/major shareholders and the liquidator. Regardless of the validity of this clearance, in the absence of independent verification, whether there are moral hazards, just from the perspective of conflict of interest, shouldn’t the relationship with several other parties also be clarified —— the independent valuation firm Deloitte, the creditor Austroid, the lithium ore buyer Hong Kong company YiHe, and the liquidator’s company McGrathNicol?

Why does the relationship with creditor Austroid also need clarification? Because theoretically, a debt loophole can exist here. For example, now inflate the debt, transfer the interests of shareholders to the debtor Austroid, and then after the liquidation is over, transfer these interests back to the purchaser and Mineral Resources through litigation or other arrangements. Of course, I don’t mean to accuse the purchaser and Mineral Resources of conspiring with creditor Austroid for such a debt loophole. But the liquidator needs to explain what mechanism can prevent such vicious events from happening. In addition, the current debt amount is still undisclosed. Why?

[2]

Announcement Section 5 (a to g) lists a total of seven reasons asking SGX to exempt the responsibility to comply with Section B of the Catalist Rules.

Part of reason a says that under Australian law, liquidators can sell Alita’s movable and immovable property without the consent of any third party (including shareholders) after obtaining creditors’ approval.

“The Liquidators do not require any other consent of any third party (including Shareholders) to perform their duties.”

Here the liquidator needs to clarify whether the so-called third party also includes SGX.

If so, it means that they can act solely based on Australian law without SGX’s consent. Then it conflicts with section 3.3, which clearly states that the sale of Alita is subject to one of two prerequisites, namely SGX’s consent to the exemption clause or Alita’s delisting.

If not included, that is, as a company listed in Singapore, Alita also needs to be subject to Singapore’s securities laws and regulations. Then how can you use Australian law as a reason to ask Singapore to approve the exemption clause? Singapore is a small country, but it certainly has independent sovereignty. Australian law has no reason to override Singapore. If the liquidator believes that Australian law can override Singapore, then go ahead. Why bother applying to SGX for an exemption clause to let them take the blame?

The liquidator needs to provide more compelling reasons to apply for the exemption.

Part of reason b claims that the transaction with the purchaser and Mineral Resources does not harm the interests of shareholders.

“The Disposal offers the most beneficial proposal available for Shareholders in the circumstances. Other indicative approaches received by the Deed Administrators had not been considered as they offered much less favourable terms, were not practicable in terms of implementation and/or lacked execution certainty.”

The liquidator believes that the current transaction arrangement is the optimal arrangement, and other companies’ proposals were not accepted by the liquidator for three reasons:

· The terms were significantly unfavourable

· The terms lack operational feasibility

· Lack of execution certainty

First of all, we highly appreciate that the liquidator has used these three aspects as selection criteria, reflecting their professionalism.

As investors, we hope the liquidator can disclose more information: in addition to Mineral Resources mentioned in the announcement, which companies have made proposals and which of the above reasons caused them to lose out?

To illustrate, under what circumstances would a proposal be considered infeasible?

Alita has not conducted exploration activities for more than five years. If the proposing party proposes to engage a third party to further explore the minerals and ascertain more reserves before valuation and liquidation, would it be considered infeasible and rejected? For an early-stage mine, is their proposal asking too much?

Speaking of lack of execution certainty, this is what we are most concerned about. Which companies were ruled out for violating this clause, while ACN 669 538 809 Pty Ltd and Mineral Resources’ proposals were accepted? However, we can see in Section 3.3 that the transaction is also subject to a prerequisite. Does this prerequisite also imply that they face the same certainty of execution issues?

Reasons d/e claim that failure to promptly approve the exemption clause may miss the opportunity to transact with Mineral Resources, and delay will impair Alita’s net assets. In fact, this statement has some uncertainty. The value of lithium resources is affected by many factors, including supply and demand balance, technological progress, etc. If shareholders’ interests cannot be reasonably protected under current circumstances, why should they cooperate to accelerate processing just for the sake of Mineral Resources and their subsidiary ACN 669 538 809 Pty Ltd whose name contains a string of numbers?

Part f of the reason claims that under the current situation of Alita, it is difficult and expensive to convene a shareholders’ meeting, and approving the exemption clause saves the most money.

We recognize the liquidator’s consideration of expenses. What we want to know is whether there are more economical and convenient channels than shareholders’ meetings, such as the Internet, to allow direct communication between the liquidator and shareholders to raise doubts and explain questions.

Part g of the reason says that the principle of creditors being compensated before shareholders in liquidation can be realized.

We strongly agree that debt precedes equity, but we cannot accept the possibility of a debt loophole as mentioned earlier. In theory, this is where a debt loophole can exist. For example, now inflating the debt transfers the interests of shareholders to the debtor Austroid, and then after the liquidation is over, transfer these interests back to the purchaser and Mineral Resources through litigation or other arrangements.

Rushing to require SGX to approve the exemption clause, this hasty approach of counting chicks before they hatch is suspecting.

[3]

In section 3.2 d, the valuation mechanism contains a payment amount calculated based on whether the existing sales agreement remains in effect.

“a mechanism for calculating a further amount payable depending upon whether the existing offtake agreement remains in place”.

My understanding is that the so-called existing offtake agreement refers to the Chinese company, that is, the sales agreement between Austroid and its affiliated Hong Kong company YiHe, which was criticized by Australian Justice Jenni Hill in court on March 28 this year. Under this agreement, Alita continued to supply lithium ore to YiHe at one-third of the market price as lithium resource prices soared tenfold, leaving Alita with wafer thin profit (the judge’s original words).

Therefore, Justice Hill ordered that in the face of soaring lithium prices and the company’s valuation from zero to A$1.5 billion, shareholders have the right to safeguard their own interests.

My understanding is that since according to the court developments on September 27, the DOCA was abolished and Alita has been freed from the control of creditor Austriod, the sales agreement between Austroid and YiHe is no longer valid. If there is any dispute, it is between the two Chinese companies Austroid and YiHe.

Continuing to execute the agreement can only mean continuing to dump at low prices, continuing to illegally transfer benefits to Hong Kong’s YiHe, and continuing to evade Australian mining taxes.

Of course, these illegal transfers of benefits to YiHe and evaded taxes can be recovered through litigation or other arrangements after Mineral Resources completes the acquisition of Alita. But by then it would only be credited to Mineral Resources and the Australian Treasury, and irrelevant to Alita’s existing shareholders.

So what mechanism is there to compensate Alita’s existing shareholders?

They are victims of dirty deeds, but those who benefit in the end may only be Mineral Resources.

[4]

Section 3.2 e of the valuation mechanism also contains taxes related to the Alita transaction payable by Alita.

“provision for further adjustments depending on the tax liabilities of Alita in connection with the transaction”

My understanding is that the transaction here refers only to the sale of assets to the proposing party during this liquidation process. If so, paying taxes according to law is reasonable.

However, one point needs to be stated. The taxes involved in transactions between the time Alita was taken over by the creditor Chinese company Austoid in 2019 and the lifting of the takeover on September 27 this year should be handled by the creditor because they were under the distorted contract operated by the creditor. If Alita has to pay additional mining taxes derived from the distorted contract, it will further transfer shareholders’ interests to YiHe or Austroid and may or may not eventually fall into Mineral Resources’ hands, because according to section 1 (c), the right to recover will also be transferred to the acquiring party in Alita’s liquidation transaction.

Once such transfer of interests occurs, shareholders would be double victims.

[5]

The first sentence of Section 6 states that the liquidator is currently unable to provide relevant calculations in tabular form according to Rule 1006 of the Catalist Rules of SGX.

“The Liquidators are currently not in a position to set out the relative figures for the Disposal computed based on Rule 1006 of the Catalist Rules.”

The liquidator explained that Alita’s audited financial reports (December 2018) and independent expert reports (August 2019, August 2021) were too long ago and may not reflect the current value of Alita.

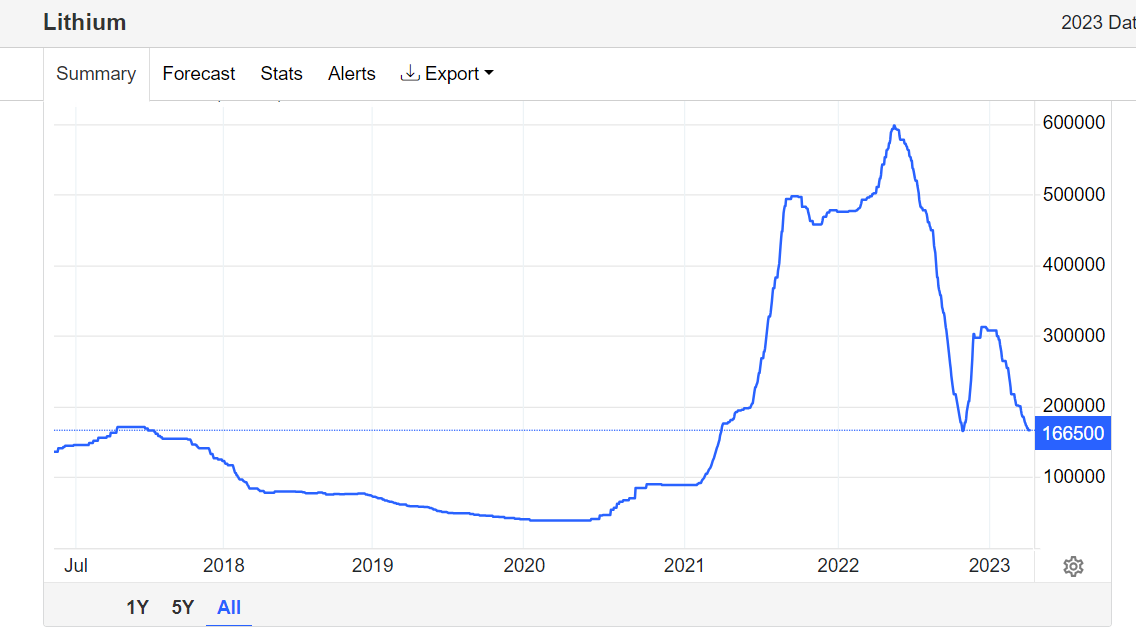

This statement makes sense. From the chart below,

In December 2018, August 2019, August 2021, the price of lithium carbonate per ton was about 70,700 RMB, 31,800 RMB, 88,000 RMB respectively. After that, it entered a soaring stage. From September 2019 to now, the price per ton ranges from 166,000 to 600,000.

The increase is huge. It can also be seen that Austroid and YiHe did transfer a lot of dirty interests (congratulations to Mineral Resources’ legal team, there will be a lot more business later).

The recent decline in lithium carbonate prices and the Midas Mineral share price plunging from 0.43 in August to below 0.15 show that large institutions are playing tricks, after all they have the power to overturn clouds and rain, for example, Mineral Resources’ Chinese partner Ganfeng Lithium has huge market pricing power.

Note: According to section 2.1 of the announcement, Alita owns 11.33% of Midas Mineral. Therefore, specifically suppressing Midas Mineral during Alita’s valuation is also a plot.

We cannot grasp the overturning of clouds and rain in the market. As shareholders of Alita, we also have doubts about the valuation background provided by the liquidator. Why does the announcement repeatedly mention that under Parents DOCA, investors will receive zero consideration, when Parents DOCA has already been abolished?

Why in Section 6 choose to give the outdated 2018 figures instead of mentioning more recent data such as the A$1.5 billion valuation obtained by the court in March 2023?

When the valuation data is still in the black box, when Rule 1006 of the Catalist Rules has not yet been complied with, why urge SGX to urgently approve the exemption clause? Can’t you wait until the valuation data comes out and SGX-related agencies evaluate whether it is fair and reasonable before deciding whether to exempt it?

Alita has a large amount of proven and yet-to-be-proven lithium reserves and thus a big cake. Many parties want to profit exclusively from it. Austroid/YiHe, the unscrupulous Chinese companies, have already put on a show.

Next, we have to see the table manners of Australian companies, Australian liquidators, and various other related parties.

Alita not only involves the interests of tens of thousands of Australian and Singaporean investors but has also received extensive attention from international media and public opinion. Its final compensation, how it is handled, relates to Australia’s honour, relates to investors’ confidence in Australia’s judicial environment, relates to investors’ confidence in Australian stock exchanges and Australian companies, and of course also the confidence in judicial liquidators.

Pay attention to your table manners, public opinion is watching you.

The three liquidators: Robert Michael Kirman, Robert Conry Brauer and Matthew Wayne Caddy

Your names are likely to be preserved in documents for a long time, cherish them.

Final Summary:

Our demands:

1. Disclose more information about the purchaser ACN 669 538 809 Pty Ltd, including its date of incorporation, registered capital, directors/senior management.

2. According to SGX Catalist Rule 1006, the valuation data should be released and evaluated by relevant SGX institutions for fairness before deciding whether to approve the waiver clause.

3. The proposer should clarify its relationship with several other parties – independent valuator Deloitte, creditor Austroid, lithium purchaser YiHe from Hong Kong, liquidator from McGrathNicol.

4. Disclose the current debt amount and composition of Alita and explain mechanisms to prevent debt entrapment.

5. What capacity expansions and costs were undertaken by Alita during the time it was seized by creditor Austroid? How many shipments and tonnage of lithium were exported and at what unit/total prices?

6. The liquidator should explain whether a third party was introduced for further exploration before liquidation, and what difficulties this poses.

7. Disclose which other companies aside from Mineral Resources and its subsidiaries made proposals, and why each was rejected for lack of feasibility or certainty. Specifically explain why their proposals were considered infeasible or lacking in implementation certainty.

The proposal from ACN 669 538 809 Pty Ltd and Mineral Resources was accepted, but section 3.3 also sets precedent conditions. Do these conditions also imply they face issues with implementation certainty?

Time to check the table manner of Australians

Alita’ abundant lithium resources make it a tempting target in the eyes of unscrupulous characters. Since the knowing of the lithium mine, it has faced lawsuits constantly. Along the way, it has experienced Jonathan Lim, Tjandra Adi Pramoko, and years of litigation between Austroid and Canaccord. After repeated twists and turns, it was originally thought that with the court ruling on September 27, 2023, in Australia, everything would settle down and Australian and Singaporean investors could get reasonable returns for a peaceful year.

Unexpectedly, a new announcement came out on October 2nd, a new company ACN 669 538 809 Pty Ltd as the purchaser appeared, the previously frequently mentioned Mineral Resources retreated behind the scenes and became the guarantor. At the same time, Deloitte was appointed to conduct valuation and issue an Independent Expert Report. However, in the situation where many questions have not been well clarified, it hurriedly set a timetable, requiring SGX to approve an exemption clause or delist Alita before October 27.

Under the current circumstances, delisting Alita will obviously make communication between investors and the company more difficult, which does not conform to SGX’s position of protecting small and medium investors and will also damage investors’ confidence in SGX.

Section B of the SGX Catalist Rules has clear requirements that selling the company requires shareholder approval. So once the requirement is exempted, investors will almost be removed from the game, with no chance to speak for their own interests in the contest concerning themselves.

In the fifth section of the announcement, a lot of space is used to explain the rationality of applying for the exemption clause. We understand the eager mood of the liquidator who sees profit coming. But as investors, we also have the right to demand more transparency and more in-depth explanations to resolve our doubts. Although it is difficult for Alita to hold a shareholder meeting under the current circumstances, it cannot be used as an excuse to close other possible communication channels.

As an investor, I have the following questions. I hope SGX can help us clarify them when responding to the Australian liquidator’s application for an exemption clause:

[1]

The first line of Section 2.2 of the announcement claims that the information about the purchaser and Mineral Resources in this section is provided by them, and the liquidator has not independently verified the accuracy and correctness of the relevant information.

We want to know whether the liquidator thinks the accuracy of the relevant information provided by the purchaser and Mineral Resources is unimportant at all?

If so, please explain why it is unimportant.

If not, please explain the difficulties in independent verification, and request the disclosing parties to provide more information for investors, media, and public to participate in verification together.

We note that the information provided by the purchaser and Mineral Resources is very limited. More needs to be supplemented in two aspects. The first aspect is more information about the purchaser ACN 669 538 809 Pty Ltd, such as its establishment time, registered capital, list of directors/executives. This information will help verify their subsequent claims. The purchaser’s name is so stylish and digital. In case it is just a short-lived existence purely for the parent company to do unspeakable things, then its directors/executives’ information is even more important and needs to be disclosed for future accountability.

The second aspect is that the relevant information provided by the purchaser and Mineral Resources only clears that they do not hold Alita’s shares and are not related to Alita’s directors/major shareholders, nor have they had any private transactions or arrangements with Alita’s directors/major shareholders and the liquidator. Regardless of the validity of this clearance, in the absence of independent verification, whether there are moral hazards, just from the perspective of conflict of interest, shouldn’t the relationship with several other parties also be clarified —— the independent valuation firm Deloitte, the creditor Austroid, the lithium ore buyer Hong Kong company YiHe, and the liquidator’s company McGrathNicol?

Why does the relationship with creditor Austroid also need clarification? Because theoretically, a debt loophole can exist here. For example, now inflate the debt, transfer the interests of shareholders to the debtor Austroid, and then after the liquidation is over, transfer these interests back to the purchaser and Mineral Resources through litigation or other arrangements. Of course, I don’t mean to accuse the purchaser and Mineral Resources of conspiring with creditor Austroid for such a debt loophole. But the liquidator needs to explain what mechanism can prevent such vicious events from happening. In addition, the current debt amount is still undisclosed. Why?

[2]

Announcement Section 5 (a to g) lists a total of seven reasons asking SGX to exempt the responsibility to comply with Section B of the Catalist Rules.

Part of reason a says that under Australian law, liquidators can sell Alita’s movable and immovable property without the consent of any third party (including shareholders) after obtaining creditors’ approval.

“The Liquidators do not require any other consent of any third party (including Shareholders) to perform their duties.”

Here the liquidator needs to clarify whether the so-called third party also includes SGX.

If so, it means that they can act solely based on Australian law without SGX’s consent. Then it conflicts with section 3.3, which clearly states that the sale of Alita is subject to one of two prerequisites, namely SGX’s consent to the exemption clause or Alita’s delisting.

If not included, that is, as a company listed in Singapore, Alita also needs to be subject to Singapore’s securities laws and regulations. Then how can you use Australian law as a reason to ask Singapore to approve the exemption clause? Singapore is a small country, but it certainly has independent sovereignty. Australian law has no reason to override Singapore. If the liquidator believes that Australian law can override Singapore, then go ahead. Why bother applying to SGX for an exemption clause to let them take the blame?

The liquidator needs to provide more compelling reasons to apply for the exemption.

Part of reason b claims that the transaction with the purchaser and Mineral Resources does not harm the interests of shareholders.

“The Disposal offers the most beneficial proposal available for Shareholders in the circumstances. Other indicative approaches received by the Deed Administrators had not been considered as they offered much less favourable terms, were not practicable in terms of implementation and/or lacked execution certainty.”

The liquidator believes that the current transaction arrangement is the optimal arrangement, and other companies’ proposals were not accepted by the liquidator for three reasons:

· The terms were significantly unfavourable

· The terms lack operational feasibility

· Lack of execution certainty

First of all, we highly appreciate that the liquidator has used these three aspects as selection criteria, reflecting their professionalism.

As investors, we hope the liquidator can disclose more information: in addition to Mineral Resources mentioned in the announcement, which companies have made proposals and which of the above reasons caused them to lose out?

To illustrate, under what circumstances would a proposal be considered infeasible?

Alita has not conducted exploration activities for more than five years. If the proposing party proposes to engage a third party to further explore the minerals and ascertain more reserves before valuation and liquidation, would it be considered infeasible and rejected? For an early-stage mine, is their proposal asking too much?

Speaking of lack of execution certainty, this is what we are most concerned about. Which companies were ruled out for violating this clause, while ACN 669 538 809 Pty Ltd and Mineral Resources’ proposals were accepted? However, we can see in Section 3.3 that the transaction is also subject to a prerequisite. Does this prerequisite also imply that they face the same certainty of execution issues?

Reasons d/e claim that failure to promptly approve the exemption clause may miss the opportunity to transact with Mineral Resources, and delay will impair Alita’s net assets. In fact, this statement has some uncertainty. The value of lithium resources is affected by many factors, including supply and demand balance, technological progress, etc. If shareholders’ interests cannot be reasonably protected under current circumstances, why should they cooperate to accelerate processing just for the sake of Mineral Resources and their subsidiary ACN 669 538 809 Pty Ltd whose name contains a string of numbers?

Part f of the reason claims that under the current situation of Alita, it is difficult and expensive to convene a shareholders’ meeting, and approving the exemption clause saves the most money.

We recognize the liquidator’s consideration of expenses. What we want to know is whether there are more economical and convenient channels than shareholders’ meetings, such as the Internet, to allow direct communication between the liquidator and shareholders to raise doubts and explain questions.

Part g of the reason says that the principle of creditors being compensated before shareholders in liquidation can be realized.

We strongly agree that debt precedes equity, but we cannot accept the possibility of a debt loophole as mentioned earlier. In theory, this is where a debt loophole can exist. For example, now inflating the debt transfers the interests of shareholders to the debtor Austroid, and then after the liquidation is over, transfer these interests back to the purchaser and Mineral Resources through litigation or other arrangements.

Rushing to require SGX to approve the exemption clause, this hasty approach of counting chicks before they hatch is suspecting.

[3]

In section 3.2 d, the valuation mechanism contains a payment amount calculated based on whether the existing sales agreement remains in effect.

“a mechanism for calculating a further amount payable depending upon whether the existing offtake agreement remains in place”.

My understanding is that the so-called existing offtake agreement refers to the Chinese company, that is, the sales agreement between Austroid and its affiliated Hong Kong company YiHe, which was criticized by Australian Justice Jenni Hill in court on March 28 this year. Under this agreement, Alita continued to supply lithium ore to YiHe at one-third of the market price as lithium resource prices soared tenfold, leaving Alita with wafer thin profit (the judge’s original words).

Therefore, Justice Hill ordered that in the face of soaring lithium prices and the company’s valuation from zero to A$1.5 billion, shareholders have the right to safeguard their own interests.

My understanding is that since according to the court developments on September 27, the DOCA was abolished and Alita has been freed from the control of creditor Austriod, the sales agreement between Austroid and YiHe is no longer valid. If there is any dispute, it is between the two Chinese companies Austroid and YiHe.

Continuing to execute the agreement can only mean continuing to dump at low prices, continuing to illegally transfer benefits to Hong Kong’s YiHe, and continuing to evade Australian mining taxes.

Of course, these illegal transfers of benefits to YiHe and evaded taxes can be recovered through litigation or other arrangements after Mineral Resources completes the acquisition of Alita. But by then it would only be credited to Mineral Resources and the Australian Treasury, and irrelevant to Alita’s existing shareholders.

So what mechanism is there to compensate Alita’s existing shareholders?

They are victims of dirty deeds, but those who benefit in the end may only be Mineral Resources.

[4]

Section 3.2 e of the valuation mechanism also contains taxes related to the Alita transaction payable by Alita.

“provision for further adjustments depending on the tax liabilities of Alita in connection with the transaction”

My understanding is that the transaction here refers only to the sale of assets to the proposing party during this liquidation process. If so, paying taxes according to law is reasonable.

However, one point needs to be stated. The taxes involved in transactions between the time Alita was taken over by the creditor Chinese company Austoid in 2019 and the lifting of the takeover on September 27 this year should be handled by the creditor because they were under the distorted contract operated by the creditor. If Alita has to pay additional mining taxes derived from the distorted contract, it will further transfer shareholders’ interests to YiHe or Austroid and may or may not eventually fall into Mineral Resources’ hands, because according to section 1 (c), the right to recover will also be transferred to the acquiring party in Alita’s liquidation transaction.

Once such transfer of interests occurs, shareholders would be double victims.

[5]

The first sentence of Section 6 states that the liquidator is currently unable to provide relevant calculations in tabular form according to Rule 1006 of the Catalist Rules of SGX.

“The Liquidators are currently not in a position to set out the relative figures for the Disposal computed based on Rule 1006 of the Catalist Rules.”

The liquidator explained that Alita’s audited financial reports (December 2018) and independent expert reports (August 2019, August 2021) were too long ago and may not reflect the current value of Alita.

This statement makes sense. From the chart below,

In December 2018, August 2019, August 2021, the price of lithium carbonate per ton was about 70,700 RMB, 31,800 RMB, 88,000 RMB respectively. After that, it entered a soaring stage. From September 2019 to now, the price per ton ranges from 166,000 to 600,000.

The increase is huge. It can also be seen that Austroid and YiHe did transfer a lot of dirty interests (congratulations to Mineral Resources’ legal team, there will be a lot more business later).

The recent decline in lithium carbonate prices and the Midas Mineral share price plunging from 0.43 in August to below 0.15 show that large institutions are playing tricks, after all they have the power to overturn clouds and rain, for example, Mineral Resources’ Chinese partner Ganfeng Lithium has huge market pricing power.

Note: According to section 2.1 of the announcement, Alita owns 11.33% of Midas Mineral. Therefore, specifically suppressing Midas Mineral during Alita’s valuation is also a plot.

We cannot grasp the overturning of clouds and rain in the market. As shareholders of Alita, we also have doubts about the valuation background provided by the liquidator. Why does the announcement repeatedly mention that under Parents DOCA, investors will receive zero consideration, when Parents DOCA has already been abolished?

Why in Section 6 choose to give the outdated 2018 figures instead of mentioning more recent data such as the A$1.5 billion valuation obtained by the court in March 2023?

When the valuation data is still in the black box, when Rule 1006 of the Catalist Rules has not yet been complied with, why urge SGX to urgently approve the exemption clause? Can’t you wait until the valuation data comes out and SGX-related agencies evaluate whether it is fair and reasonable before deciding whether to exempt it?

Alita has a large amount of proven and yet-to-be-proven lithium reserves and thus a big cake. Many parties want to profit exclusively from it. Austroid/YiHe, the unscrupulous Chinese companies, have already put on a show.

Next, we have to see the table manners of Australian companies, Australian liquidators, and various other related parties.

Alita not only involves the interests of tens of thousands of Australian and Singaporean investors but has also received extensive attention from international media and public opinion. Its final compensation, how it is handled, relates to Australia’s honour, relates to investors’ confidence in Australia’s judicial environment, relates to investors’ confidence in Australian stock exchanges and Australian companies, and of course also the confidence in judicial liquidators.

Pay attention to your table manners, public opinion is watching you.

The three liquidators: Robert Michael Kirman, Robert Conry Brauer and Matthew Wayne Caddy

Your names are likely to be preserved in documents for a long time, cherish them.

Final Summary:

Our demands:

1. Disclose more information about the purchaser ACN 669 538 809 Pty Ltd, including its date of incorporation, registered capital, directors/senior management.

2. According to SGX Catalist Rule 1006, the valuation data should be released and evaluated by relevant SGX institutions for fairness before deciding whether to approve the waiver clause.

3. The proposer should clarify its relationship with several other parties – independent valuator Deloitte, creditor Austroid, lithium purchaser YiHe from Hong Kong, liquidator from McGrathNicol.

4. Disclose the current debt amount and composition of Alita and explain mechanisms to prevent debt entrapment.

5. What capacity expansions and costs were undertaken by Alita during the time it was seized by creditor Austroid? How many shipments and tonnage of lithium were exported and at what unit/total prices?

6. The liquidator should explain whether a third party was introduced for further exploration before liquidation, and what difficulties this poses.

7. Disclose which other companies aside from Mineral Resources and its subsidiaries made proposals, and why each was rejected for lack of feasibility or certainty. Specifically explain why their proposals were considered infeasible or lacking in implementation certainty.

The proposal from ACN 669 538 809 Pty Ltd and Mineral Resources was accepted, but section 3.3 also sets precedent conditions. Do these conditions also imply they face issues with implementation certainty?

8. Propose channels besides the shareholder meeting for the liquidator to directly communicate with shareholders to address concerns.

9. After the DOCA was terminated, Alita was released from creditor Austroid. Is the offtake agreement between Austroid and YiHe still in effect?

10. Please elaborate on the selection process for the independent third-party valuator. Since Deloitte has already produced reports in previous legal proceedings, please explain in detail why it was selected again this time.